Statistics indicate that the number of divorced persons is steadily rising in Canada, increasing from an estimated 1.88 million in 2000 to 2.78 million in 2022. This means a significant portion of the population is suffering from financial setbacks that come with separation, including matters like the division of assets as well as pension entitlements after separation.

This article provides insight into the laws and regulations governing spousal entitlement to pension upon divorce in Canada, shedding light on the conditions, considerations, and types of pension plans for ex-partners.

Understanding Pensions in the Context of Divorce

In Canada, pensions are legally recognized as a shared asset during marriage. This means they are subject to division during divorce proceedings. Both partners are considered contributors to the pension, regardless of who was the primary earner.

Determining the exact split of pension after divorce can be complicated due to the legalities and complexities involved. This involves figuring out the current pension value while also considering future benefits. It is essential to understand that provincial laws govern the specific procedures for pension division, but the basic principle of equitable distribution remains the same nationwide.

Conditions of Spouse Entitlement to Pension After Divorce in Canada

Conditions to determine whether an ex-spouse can claim a portion of the retirement depends on the nature of the relationship given as follows:

- Married Spouses: When the married couple divorces, the splitting of pension is usually straightforward. The court considers specific factors of marriage, for instance, the length of marriage, and then orders for the division of assets accordingly.

- Common Law Spouses: Couples who live together for more than 2 years in a marriage-like relationship might also qualify for pension-sharing. However, they need to normally recognize each other’s rights to these benefits. This means that if you were married or lived together like a couple for at least a year, the general rule of a 50/50 split of the value applies to the partners that were earned during that time.

Considerations for Spousal Entitlement

Several factors can impact the division of pension during a divorce, some of which are mentioned below.

- Length of the Marriage: The length of the marriage can influence how a pension is divided, with longer marriages often leading to a more equal division of pension assets.

- Contribution to the Marriage: The contributions of both partners to the marriage, both financial and non-financial contributions, are considered when dividing pensions. The nonfinancial contributions include caretaking, homemaking, and supporting spouse’s careers.

- Age and Health of Spouses: The age and health of each spouse can affect the division of pensions, particularly when calculating the expected retirement age and life expectancy rate.

- Assets: Pension division is often also related to the division of marital possessions like the house, investment, and savings. To be fair, the pension’s value might be equated against other assets.

- Pre-existing Agreements: Prenuptial or postnuptial agreements may impact the division of pensions, depending on the terms outlined in the agreements.

Provincial Differences in Pension Division Laws

While the general principle of pension division remains consistent across Canada, each province has specific legislation that affects how pensions are divided during divorce. Understanding your provincial laws is crucial for determining your rights and the division process.

Ontario’s Family Law Act

In Ontario, pensions are treated as family property under the Family Law Act. The province follows the equalization principle, meaning the spouse with higher net family property must pay half the difference to the other spouse.

This means that if your pension value increased by $100,000 during the marriage, and your spouse’s assets increased by $60,000, you would owe them $20,000 to equalize the difference. However, the pension itself doesn’t need to be divided directly – the value can be offset against other assets like the family home.

British Columbia’s Framework

British Columbia’s Family Law Act considers pensions as family property that can be divided at the date of separation or at retirement. This gives couples more flexibility in how they handle pension division.

For example, if you’re a member of BC’s Teachers’ Pension Plan, your former spouse can become a “limited member” and receive their share directly from the plan once you reach retirement age.

Quebec’s Unique Approach

Quebec operates differently under its Civil Code. Instead of splitting the entire pension, Quebec focuses on the contributions made during the marriage. When pension benefits are eventually paid out, they’re divided based on each spouse’s proportional contributions during the relationship.

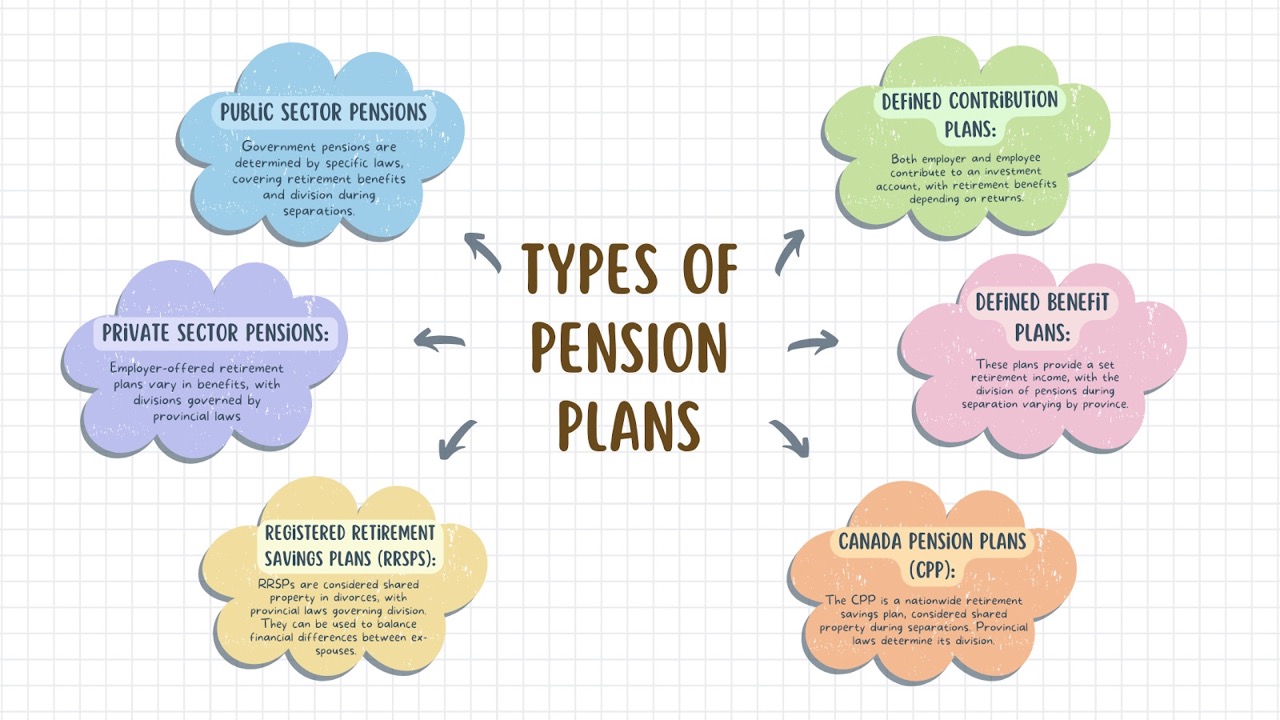

Types of Pension Plans Subject to Separation

The legal framework of property division upon divorce in Canada is primarily governed by provincial and territorial family act laws, as well as federal jurisdictions for certain types of pensions. For instance in Ontario, the division of pensions is governed by the Family Law Act.

There are various types of pensions subject to division upon divorce, including:

Public Sector Pensions

Public sector pensions include the pensions that are provided to federal, provincial, or municipal employees. These pensions are specified by certain laws that explain how much money people will get when they retire and how it gets divided if spouses get separated.

For federal public sector pensions, such as those under the Public Service Superannuation Act, the Pension Benefits Division Act governs the division.

Private Sector Pensions

Private sector pensions are retirement savings plans offered by employers. Unlike government pensions, these plans vary widely regarding benefits and how they get structured. Specific pension plan rules and provincial family law govern these pensions.

Defined Contribution Plans

These pension plans work like saving accounts. With a Defined Contribution Plan, both the employer and employee contribute money to an investment account. Pension benefits that come from returns on those investments are directly added to the account, and after retirement now the member has several choices regarding what to do with these funds.

This money can be used to buy a steady income, keep it invested and withdraw as per requirement, or transfer the amount to a registered plan. If you decide to keep the funds in the original account, your spouse can immediately claim their share, which is transferred to a new account under their name.

Defined Benefit Plans

Defined Benefit Pension plans offer a specific retirement income based on factors like the number of years served and earnings. When a couple separates, the non-pensioned spouse often has rights to a portion of the pension built up during marriage. The framework followed to divide the financial assets however varies from province to province.

The employer bears the investment risks in these plans. Examples include government pensions and some workplace pensions.

Canada Pension Plans

The Canadian Pension Plan (CPP) is a retirement savings plan that is available to most Canadian workers. If the couple breaks up, it is considered that the money earned through the CPP belongs to both partners. However, division is done by the law in your province. Some provinces in Canada have laws that would automatically split CPP equally between former partners, while some would leave the decision in the hands of a judge.

For instance, British Colombia’s Family Law Act considers pension as family property. This act allows for the division of the pension’s value at the date of separation or the pension is divided at the time of retirement.

However, another province, Quebec, follows a different approach under its Civil Code. Instead of splitting the entire pension, the province focuses on the money earned during the marriage. So when the pension is paid out, it’s divided based on each spouse’s contributions.

Registered retirement saving plans

When a couple separates or divorces in Canada, their shared assets, including retirement savings, must be divided. Registered Retirement Saving Plans (RRSPs) are generally considered shared property and are subject to division as per specific provincial laws.

While contributions made solely by one spouse are often excluded, any growth in the RRSP’s value during the marriage is typically shared. Additionally, RRSPs can be used to balance out financial differences between ex-spouses, when there is no direct entitlement.

Determining the Value of Pension

Valuing the pension is a significant aspect of dividing the pension assets during the divorce process. This is influenced by several factors, such as a pension plan, the age of the pension holder, and the rate at which you are expected to retire.

There are two primary methods of valuing a pension:

Present Value Method

The Present Value Method represents the current value of a lump sum compared with the future pension payments, which are based on the consideration of the life expectancy of a pension holder, interest rates, and inflation. This method is commonly used in legal systems treating pensions as marital property.

Division at Source

This method is where, at retirement, the pension is divided and each spouse receives a portion of the ongoing pension payments. It is applied in cases where pensions are not considered as marital assets but as future income.

Timeline and Critical Deadlines

Missing deadlines for pension division can cost you thousands of dollars in retirement benefits. Each type of pension has specific time limits that you must follow.

Application Deadlines by Pension Type

- CPP Credit Splitting: 48 months after separation for common-law couples; mandatory for married couples upon divorce

- Federal Public Service Pensions: No specific deadline, but division becomes more complex after retirement

- Provincial Employment Pensions: Varies by province and plan – some have 36-month limits

- Private Sector Pensions: Generally no deadline, but earlier application provides more options

Objection Periods

Once you apply for pension division, your former spouse has specific rights to object:

- 90 days to file written objection for most employment pensions

- Valid objection grounds include changed court orders, terms satisfied by other means, or ongoing legal appeals

- Waiver option – your spouse can waive their right to object in writing

It is important to note that pension division is not automatic. You must formally apply even after your divorce is finalized.

Steps Involved in Obtaining a Division of Pension Benefits

Either you or your ex-partner can request a split of pension benefits. The following steps are involved in the process:

Step 1: Request Information on the Pension Benefits Division

Before you request a pension benefits division estimate, it’s necessary to review the “Request for Estimate” section of the Division of Pension Benefits Package. This section provides details about the number of estimates allowed per year and the necessary documents and forms.

To get an estimate of the division amount before a formal application, complete the “Request for Pension Benefits Division Information (PWGSC-TPSGC 2488)” and submit it with any additional required paperwork.

Step 2: Apply for Pension Benefits Division

To formally request the division of your public service pension, you need to submit the “Application for Divison of a Public Service Superannuation Act Pension (PWGSC-TPSGC 2486)” form. Make sure to include a copy of your court order or written agreement, along with any additional required documents.

Step 3: Division of Pension Benefits

After you get the division approval, the amount of pension earned during the specified division period is transferred into a designated registered retirement savings account.

For additional information refer to the Pension Benefits Division Regulations.

Tax Implications You Need to Know

The tax consequences of pension division can significantly impact your financial situation. Understanding these implications helps you make better decisions about how to structure your division.

Transfers to Locked-in Accounts

When pension division amounts are transferred directly to locked-in RRSPs, RRIFs, or other registered accounts, you typically avoid immediate tax consequences. The taxes are deferred until your former spouse withdraws money from these accounts.

However, this creates a tax liability for your former spouse that they need to plan for in retirement.

Direct Payment Tax Consequences

If any portion of the pension division exceeds the Income Tax Act limits for registered transfers, that excess amount gets paid directly to your former spouse. When this happens:

- Income tax is automatically withheld at source

- Your former spouse receives the net amount after tax deductions

- This immediate tax hit can significantly reduce the division value

RRSP and TFSA Division Rules

RRSPs accumulated during marriage are generally subject to division, but specific transfer rules apply:

- RRSP transfers between spouses during divorce proceedings are typically tax-free

- TFSA contribution room cannot be transferred, but the funds themselves can be transferred without affecting either person’s contribution limits

- Timing matters – transfers must be part of formal divorce agreements to qualify for tax-free treatment

Key takeaways: ▪ Pensions are shared assets in Canada since both spouses contribute to the pension during marriage. ▪ Determining the split of the pension depends on various factors like marriage length, financial contributions of each spouse, and, other assets. ▪ Different pension plans (public, private, defined benefit, defined contribution, CPP, RRSP) have different rules for division. ▪ Calculating the value of the pension is often complex, involving methods like present value or division at the source. |

Frequently Asked Questions

Division of pension earned during the marriage typically depends on two things: the pension plan in place at the time of marriage and provincial family laws governing the divorce.

If the pension plan used is a defined benefit (DB) plan, the value of the pension is first calculated, with each portion being allocated according to your provincial laws. However, if the plan used is a defined contribution plan (DC), then the account balance is simply divided equally between you and your partner.

It is important to remember that pension division must be formally applied for and is not granted automatically. Since this may be a complex process, it is best to consult a legal professional before submitting your application.

Since pensions are considered marital assets, they are subject to division in the same way other properties like a house, car, and land may be evaluated during a divorce. This means that even if your pension was not addressed during the divorce settlement or separation agreement, your ex-partner might still have a claim no matter how many years have passed.

However, once the divorce is finalized, it becomes more challenging for a party to reopen the settlement. In the case of pension division, if you did not apply for division of pension credits within 36 months of the marriage ending, your ex-wife may find it difficult to claim the credits, though it would not be entirely impossible.

It’s crucial to consult with a family lawyer to understand your situation and whether your ex-spouse has any legal grounds to claim your pension.

In Ontario, Tax-free Savings Accounts (TFSAs) are treated as property during a divorce and are subject to division, like other assets.

Ontario follows the principle of equalization of net family property. This means that the increase in value of each spouse’s assets during the marriage is added up, and the spouse with the higher net increase is required to pay half of the difference to the other spouse. TFSAs are included in this calculation. However, the TFSA itself does not necessarily need to be divided directly. Instead, the value of the TFSA might be offset against other assets to achieve an equal distribution.

Keep in mind that the TFSA contribution room is not transferable between spouses, each retains their limit. However, you can transfer TFSA funds to an ex-spouse without affecting the contribution room, as long as it’s part of your divorce agreement.

In Ontario, you may need to split your Canada Pension Plan (CPP) benefits with your ex-spouse. This is mandatory for divorced couples, with common-law partners being granted a time period of 48 months after separation to apply. Your ex-partner can also choose to waive the rule in writing, in which case the credits will not be split.

CPP benefits are usually divided through a “credit splitting” process, which adjusts the CPP credits based on the time spent in the relationship and CPP contributions made during that time.

Credit splitting ensures that both partners receive a fair share of the CPP benefits based on the contributions made during the marriage, especially if one partner stayed home to care for children or otherwise contributed less directly to the workforce.

Seeking Legal Advice

Dividing pensions after divorce can be complicated. It involves legal paperwork, financial calculations, and personal factors. Because of the significant financial impact of these decisions, it’s important to get legal help from a lawyer who deals with family law practices.

If you are going through divorce proceedings, do not hesitate to reach out to Nussbaum Law. Our professionals dealing with family law will walk you through the process of financial division in your best interest. Contact us today to schedule a consultation and protect your financial future.